The key takeaways today:

- Will the $1 trillion in AI spending pay off?

- The S&P 500 may be offering a false sense of calm

- Investors face an uncertain second half of 2024

- Global forecast changes: US and UK GDP, profits in Japan

- How bullish power traders are investing in the AI boom

- A revolution among women in the workforce

- Briefings Brainteaser: In which countries do women spend the most hours on work?

Was this newsletter forwarded to you? Sign up now. |

|

|

| A skeptical look at AI investment |

|

|

Tech giants and other companies are set to spend an estimated $1 trillion on AI capex in coming years. But AI may prove far less promising than many business leaders and investors expect.

Daron Acemoglu, Institute Professor at MIT, estimates that only a quarter of AI-exposed tasks will be cost-effective to automate within the next 10 years — which means that AI will impact less than 5% of all tasks and boost US productivity by only 0.5% and GDP growth by 0.9% cumulatively over the next decade.

Truly transformative changes won't happen quickly, and few — if any — will likely occur within the next 10 years, Acemoglu says on Goldman Sachs Exchanges, which explores the latest Top of Mind report, Gen AI: Too much spend, too little benefit? “The current architecture of the large language models has proven to be more impressive than many people would have predicted, but I think it still takes a big leap of faith to say that just on this architecture of predicting next word, we're going to get something that's as smart as, you know, Hal in 2001: A Space Odyssey,” he says. “So anything that's invented — or big breakthroughs — is not going to have a huge effect within the next few years.”

|

|

|

Jim Covello, Goldman Sachs' Head of Global Equity Research, goes a step further, arguing that to earn an adequate return on the approximate $1 trillion estimated cost of developing and running AI technology, AI must be able to solve complex problems — which, he says, it isn't built to do. “We're a couple of years into this, and there's not a single thing that this is being used for that's cost-effective at this point,” he says. “I think there's an unbelievable misunderstanding of what the technology can do today. The problems that it can solve aren't big problems. There is no cognitive reasoning in this.” |

|

|

| US stocks are more volatile than you think |

|

|

|

“The S&P 500 may be giving investors a false sense of calm,” says Brian Garrett, who oversees equity execution on Goldman Sachs' cross-asset sales desk. Garrett says that while the S&P 500's dependable-looking rally is supported by strong economic data and earnings, “there is something going on under the surface.”

He points out that funds selling options have grown dramatically in size. Their sales tend to compress volatility, since the buyers of these options are market-makers who hedge their exposure by selling the index when it rises, and buying when it falls.

This behavior pushes the market into a tighter range. That's “one reason why we've seen the S&P relatively quiet, while there have been large moves in individual stocks,” Garrett says. The systematic selling of these options also drives down the prices of portfolio hedges, which rise in value when stocks decline.

“It hasn't been cheaper to hedge a portfolio in the last decade,” Garrett says. “So for those worried that volatility could return: You've got options.” |

|

|

| Easing cycles and elections make for an uncertain second half of 2024 |

|

|

Central bank cutting cycles and potential surprises from elections add extra elements of uncertainty in the second half of 2024. Goldman Sachs Asset Management's mid-year outlook examines the major themes at play, as well as the strategies that investors might consider as they navigate a dynamic environment.

In this climate, core fixed income exposure can help to build more resilient, well-diversified portfolios. Hedge funds and liquid alternatives can enhance diversification, which is important given the potential for flare-ups of market volatility and geopolitical shocks. In the equity market, small caps may be poised for a rebound after a multi-year period of underperformance versus large caps.

Private markets continue to evolve, offering multiple avenues to potentially enhance risk-adjusted returns and complement traditional investments. In private equity, operational value creation levers — revenue growth and margin expansion — are poised to become the main determinants of successful investment outcomes, Goldman Sachs Asset Management suggests. In private credit, those with the scale and flexibility to lend throughout the capital stack, as well as a deep book of existing borrowers, look best positioned.

The mid-year outlook also raises key questions related to asset classes, elections, and mega-trends, as investors prepare for the months ahead:

What is “normal” for private equity?

Some PE investors are questioning what a “normal” environment will now look like. The breakneck pace of activity in 2021-22 was likely an anomaly, fueled by historically low rates and easy access to capital. But a prolonged return to pre-pandemic trendlines might not be the most likely path forward. The size, scope, and nature of deals is likely to continue evolving, defying attempts to define “normal.”

What might the US election mean for the Inflation Reduction Act?

A repeal of the IRA, the US's signature climate policy, seems unlikely regardless of who wins office. Despite potential post-election policy shifts, Goldman Sachs Asset Management continues to expect strong growth in climate-related and low-carbon investment opportunities, driven by improved pricing for solar generation and energy efficiency.

How will AI shape real estate and infrastructure?

From a real estate perspective, the location of data center assets is critical, given the need for affordable and reliable power in the evolution of AI. Generating and delivering efficient energy will be vital in the coming years to support AI's expected growth curves. Investors with the resources and expertise to assess both halves of the supply and demand equation look best-positioned to capitalize on this megatrend.

|

|

|

| Global forecast changes: US GDP, UK GDP, profits in Japan |

|

|

|

↑↓ US: Goldman Sachs Research revised its annualized quarter-on-quarter forecast for US GDP growth to 2.6% in the second quarter of 2024, up from a previous estimate of 1.8%, based in part on the stronger-than-expected retail sales report and a spike in auto assemblies in June. For the third and fourth quarters of 2024, our analysts scaled down their forecasts to 2.4% and 2.2% respectively, from previous estimates of 3% and 2.5%.

↑ UK: In May, the UK's GDP grew by 0.4%, month on month – higher than expectations of 0.2% growth. Goldman Sachs Research raised its forecast for annual GDP growth for 2024 to 1.2% (from 1.1% previously), above the consensus view of 0.7% and the Bank of England's estimate of 0.4%.

↑↓ Japan: Goldman Sachs Research revised its earnings forecasts for the TOPIX stock index in Japan. The new forecasts call for earnings-per-share growth of 10%, 9%, and 7% in the financial years 2024, 2025, and 2026 respectively. (Earlier forecasts for 2024 and 2025 were 11% and 6% respectively.) “A cumulative 29% growth over the next three years should underpin the Japan market's move higher,” our analysts write. Data as of July 17, 2024

|

|

|

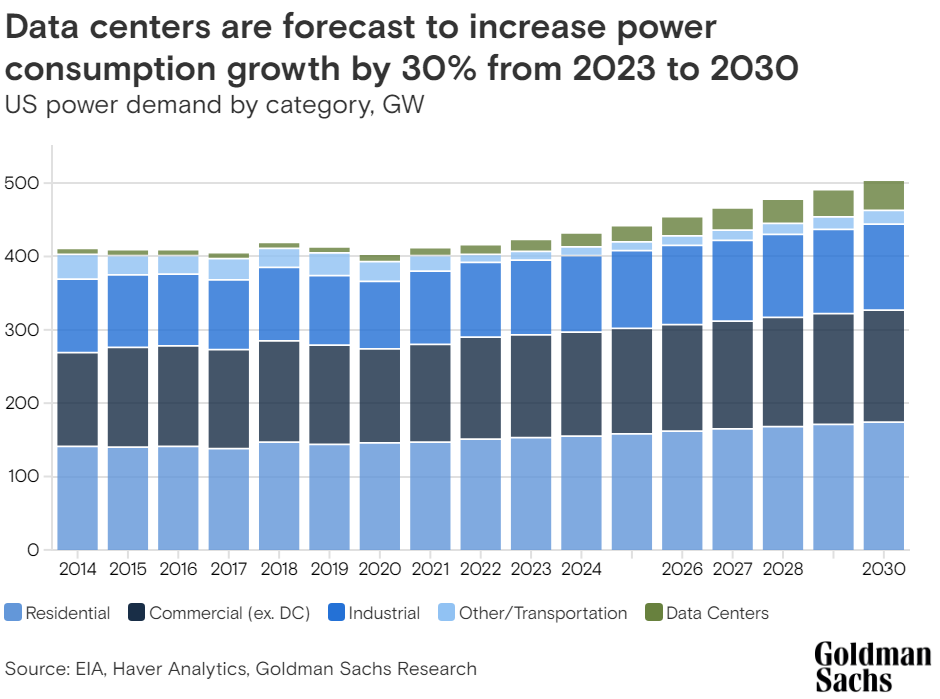

| Bullish expectations for US electricity are attracting new power traders |

|

|

A new class of traders is investing in US power markets, seeking opportunities to access the boom in generative AI, according to Sarah Kiernan, head of Americas Commodities Sales in Goldman Sachs Global Banking & Markets.

Power generation is in new focus because data centers, which provide the computing muscle to train and support AI technologies such as large language models, require a growing amount of electricity. Goldman Sachs Research analysts estimate that data center power demand will grow 165% by 2030 (as of July 9, 2024). That adds to the increasing demand for power from electric vehicles and the onshoring of manufacturing and supply chains.

|

|

|

Kiernan says Goldman Sachs is having more conversations about the power market with hedge funds and asset managers, which haven't traditionally been major players in the sector.

The cost of power on the US east coast, one of the largest and most liquid power markets, started to rise around February and March, Kiernan says. The spark spread — the difference between the wholesale market prices of electricity and the cost to produce it — has roughly doubled there as of mid-June.

US data centers are particularly concentrated in the Virginia area. Goldman Sachs Research documented a rise in commercial power consumption there of 37% from 2016 to 2023, as power demand remained roughly flat in most other states.

The power market hasn't traditionally been a mainstay for hedge funds and asset managers because it's less liquid than commodities like oil and copper, and prices tend to be harder to observe, Kiernan says. But there are signs that's changing as investors look for additional ways to invest in the AI boom. |

|

|

| How women's labor participation is reshaping the global economy |

|

|

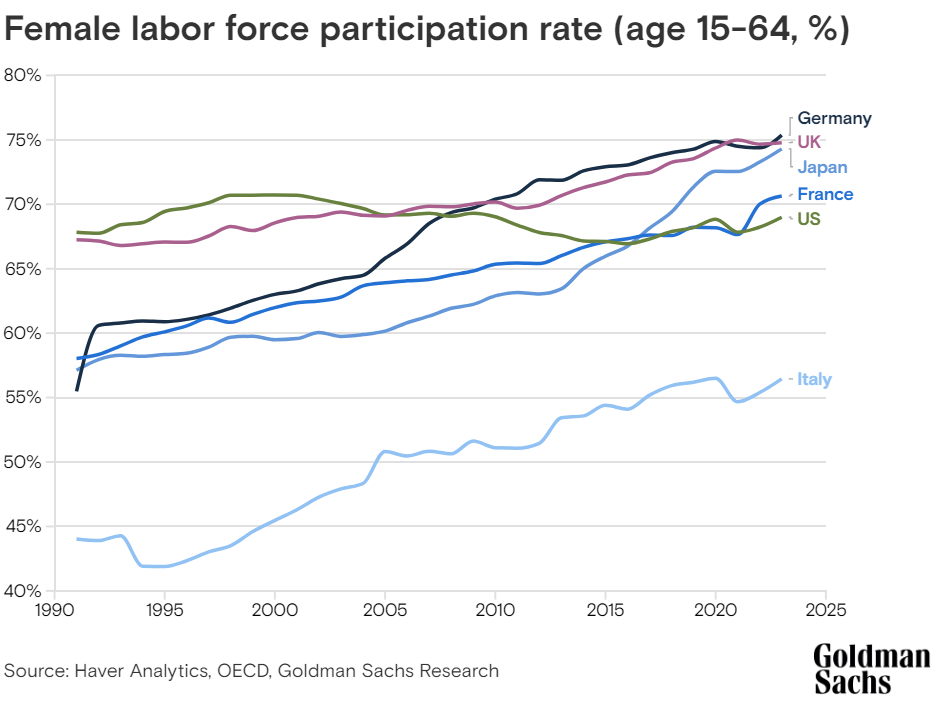

Goldman Sachs Research first published a report on women's participation in the labor force, and the economic opportunities opened up by greater participation, in 1999. Twenty-five years on, Goldman Sachs Research's Sharon Bell, senior strategist on the European Portfolio Strategy team, and analyst Yuriko Tanaka take a fresh look at those issues on a global scale.

The new report, titled "Womenomics: 25 Years and the Quiet Revolution", finds that women's labor-force participation has grown across many developed economies. Joining the workforce has offered improvements in welfare and opportunity for women, but it has also had an enormous economic impact. Italy's workforce, for example, would have shrunk if not for greater participation from women.

|

|

|

But disparities remain. Non-paid work, such as caregiving for family, takes up a larger share of a woman's day in every country, making it harder for them to reach the top echelons in firms, academia, or politics. Women are also more likely to work part-time.

Further, the lack of women in the most senior ranks of companies, especially at the executive level, is notable and persistent. There are also disparities across sectors. In the US, the share of women employees in technology and financial services (high-paying industries) has fallen.

Much remains to be done. However, there are reasons to expect women's participation in the workforce, as well as pay and opportunities at the highest ranks, to continue to increase. Women's participation fell during the pandemic but has generally more than recovered since. While pay gaps are high in older age groups, even here the gaps have narrowed slightly, and there is a steady climb on most corporate-related metrics.

Read the full report: "Womenomics: 25 Years and the Quiet Revolution."

|

|

|

| Briefings Brainteaser: Long working days |

|

|

In most countries, the total time in a day that women spend in work — paid and unpaid work combined — is higher than for men. Women in Mexico spend the highest proportion of their days on work: more than 40%. Which country comes next in the list?

A) India

B) Turkey

C) US

D) Portugal

Check the answer here. |

|

|

| Goldman Sachs in the news |

|

|

By clicking on these links, you will be redirected to external websites that Goldman Sachs does not own or operate. Goldman Sachs is not responsible for the products, services, or content provided on those sites. Please refer to each external website's terms, privacy and security policies for details. |

|

|

|

CNBC Jul 16 | | Market will see some broadening over the next six months, says Goldman Sachs' David Kostin (3:59) |

|

|

|

|