The key takeaways today:

- Investor reactions to French and UK elections couldn't be more different

- How India's services sector became an economic force

- It's cheap to hedge against a drop in US stocks ...

- ... And here are the best commodities to hedge inflation

- Decarbonization "laggards" may be an investment opportunity

- Briefings Brainteaser: Which countries have the fastest-growing services economies?

Was this newsletter forwarded to you? Sign up now. |

|

|

| Why the French and UK elections matter for investors |

|

|

|

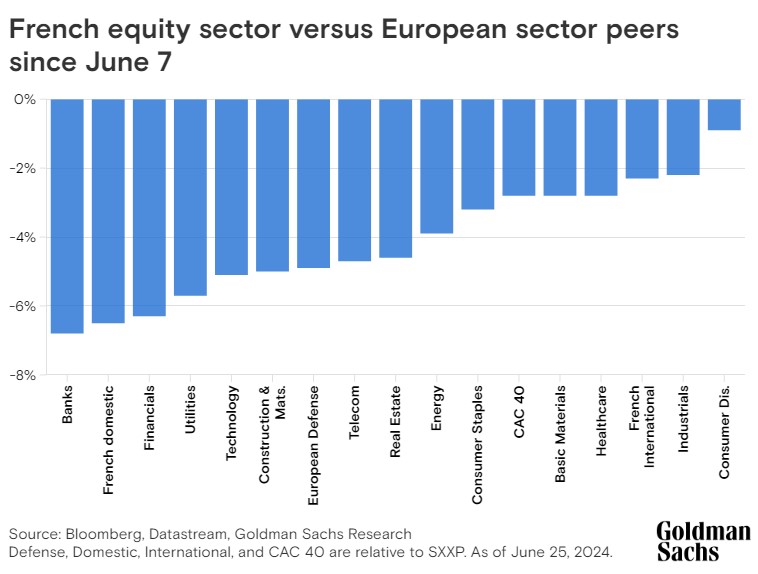

Two of Europe's three largest economies are heading to the polls, and investors' reactions couldn't be any more different. France's upcoming parliamentary elections are wreaking havoc on French stocks and bonds, while UK financial markets have been relatively stable as the country gears up for its own general election on July 4.

In France — where President Emmanual Macron called a surprise snap election that takes place on June 30 and July 7 — the market volatility has wiped out the CAC 40 index's year-to-date gains. “The reason that markets are finding it so difficult to price is that there's not a clear path to a great outcome for markets,” Sharon Bell, senior strategist on Goldman Sachs Research's European Portfolio Strategy team, says on Goldman Sachs Exchanges. |

|

|

|

One of the key concerns is whether the future French government will be able to rein in the country's already high level of debt — or continue to increase spending, notes George Cole, head of European Rates Strategy in the Global Macro and Markets Research Group. “If there is a substantial challenge to fiscal discipline coming out of the next French government, there is maybe the potential for that to have knock-on effects to other economies,” he says.

Meanwhile, investors are more sanguine about the upcoming UK election given that the outcomes appear to be more certain, with polls pointing to a Labour Party win. “Ultimately, it feels like the overall uncertainty around this election, not just for the outcome itself, but the implications for macroeconomic policy on the far side, is likely to be a bit smaller this time,” Cole says. Click here to listen to the full Exchanges podcast.

|

|

|

| How India became the world's emerging services factory |

|

|

|

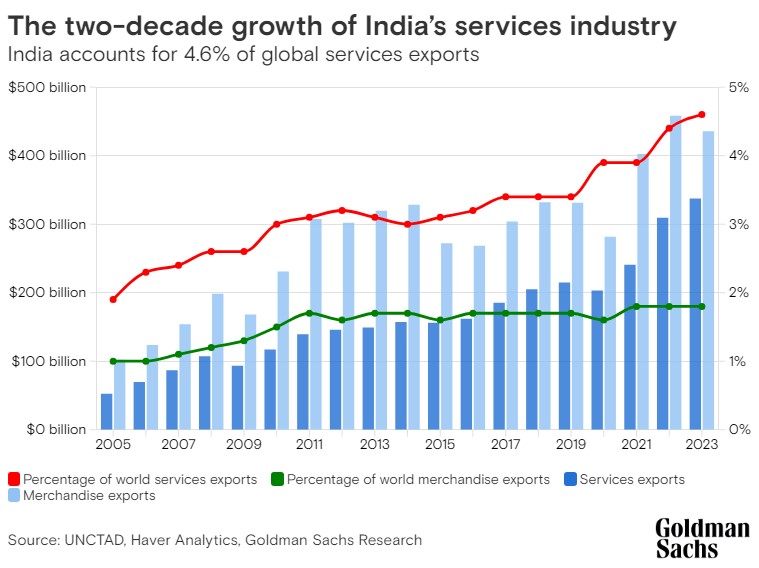

As the world has grown more wired and interconnected, countries have been able to export more kinds of services. Globally, services exports have roughly tripled since 2005, now making up 7% of the world's GDP in 2023. Only two countries' services exports grew faster than India's, according to Goldman Sachs Research.

India's services exports grew from $53 billion to $338 billion between 2005 and 2023 — almost double the rate of the rest of the world — and now form nearly a tenth of the national GDP. Its growth has outstripped that of India's exports of material goods. In their baseline forecast, our economists expect India's services exports to touch 11% of GDP by 2030, and to be valued at around $800 billion. |

|

|

-

Through the last two decades, computer services formed the dominant category in India's services exports — a dynamic that continues today. In 2023, this category made up nearly 47% of all services exports.

- The specialized services hubs that companies have opened in India are called global capability centres, and they're based overwhelmingly in the major cities. The revenues of Indian GCCs have quadrupled over the last 13 years to $46 billion in the 2023 fiscal year. The number of GCCs has more than doubled from 700 to 1,580 in that period, and the sector has added around 1.3 million employees, taking the total employee headcount to 1.7 million in the 2023 fiscal year.

|

|

|

| S&P 500 hedges have fallen to their cheapest level in five years |

|

|

|

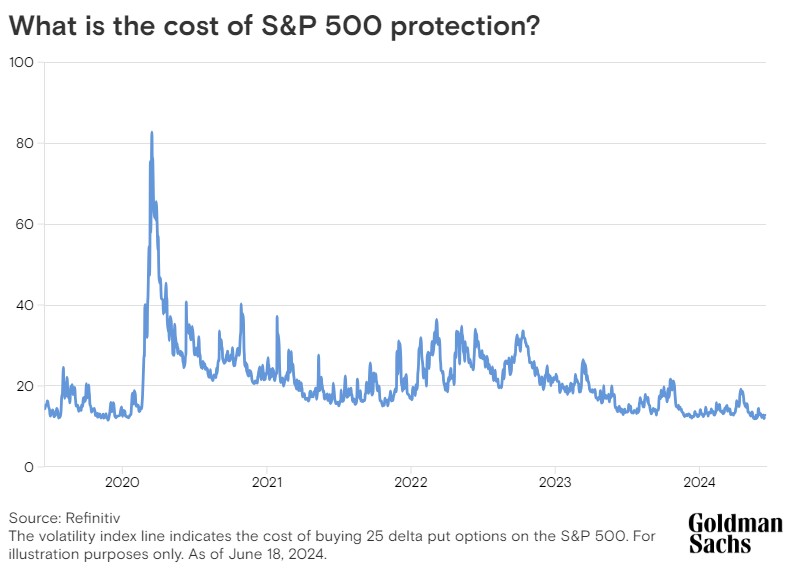

As US equity markets have repeatedly hit all-time highs this year, the cost of protecting against drops in the S&P 500 (or SPX hedging) has remained near its lowest level in the past half-decade. Investors are flocking to equities as their appetite for risk remains high, says Lindsay Matcham, who works in futures sales trading in Goldman Sachs Global Banking & Markets. “The trend line of SPX protection this year has given us an indication of the potential complacency and potential overcrowdedness of markets,” Matcham says.

Investors hedge their exposure to the S&P 500 in various ways: via over-the-counter securities or in listed markets, at an index level or via single stocks. “If you wanted to hedge your long exposure, you would buy put options on the index, which would protect you if equity valuations moved lower,” Matcham says. In previous years, during events that depressed the appetite for risk — such as the 2008 financial crisis or the onset of Covid in 2020 — the cost of SPX protection rose to multi-year highs, as equity markets tumbled and investors scrambled to protect themselves.

|

|

|

This year, amid the equity rally, the cost of “vol” — volatility, or hedges such as put options — has moved lower. “The sellers of options have made money and pocketed the premium, since there has been no vol event or sell-off,” Matcham says.

“Even if you are not overly bearish, it makes sense to buy protection for your portfolio, given how cheap vol is,” Matcham says. “We don't believe the market is sufficiently pricing the potential tail risks. These include the upcoming French elections, the US elections, potential escalations of conflict in the Middle East, and potential trade and tariff turmoil with China.” |

|

|

| Which commodities are the best hedge for inflation? |

|

|

|

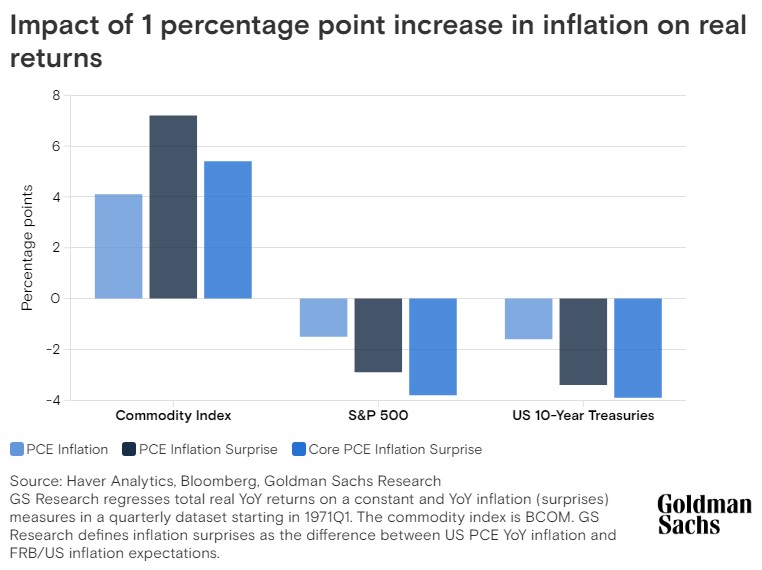

Commodities have demonstrated strong resilience in the face of inflation and have been a critical hedge for bonds and equities when prices and wages are climbing, according to Goldman Sachs Research. They may also offer protection for portfolios to volatility stemming from the US election.

A 1 percentage point surprise in US inflation has, on average, led to a real (inflation adjusted) return gain of 7 percentage points for commodities, while that same trigger caused stocks and bonds to decline 3 percentage points or more, write Daan Struyven, head of oil research in Goldman Sachs Research, and analyst Lina Thomas in the team's report. |

|

|

|

While gold, energy, agricultural products, and industrial metals tend to have provided varying levels of protection against a surprise increase in inflation, Goldman Sachs Research expects gold to provide the best hedge in the coming months versus risks from rising prices and wages and from geopolitical tumult.

|

|

|

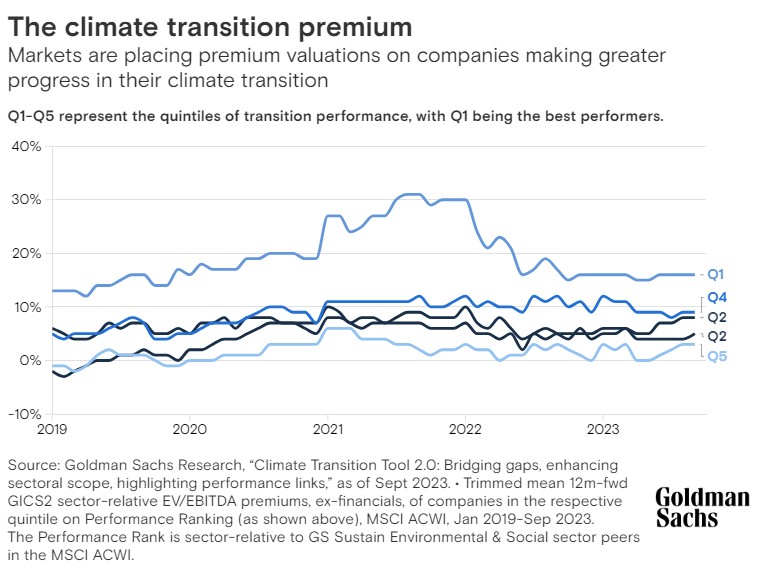

| Heavy emitters are decarbonization's undervalued stocks |

|

|

|

Climate investors have mainly focused on finding the direct “enablers” of the world's push to decarbonize, such as renewable energy firms. But investors should also pay attention to “improvers” in heavily polluting sectors, according to a report from Goldman Sachs Asset Management.

“There are many businesses that are currently perceived as transition laggards, predominantly due to the market's heavy penalization of perceived transition risk,” writes Kevin Martens, a managing director and portfolio manager in Fundamental Equity in Goldman Sachs Asset Management. “Many of these companies will still be relevant in the future green economy and may even be critical in enabling sustainability commitments.”

|

|

|

Martens points to a couple of examples of potentially compelling investment opportunities in high-emission sectors:

- Miners: Metals and mining are currently responsible for up to 7% of global greenhouse gas emissions. Mining companies could use technology to reduce their costs and make progress on decarbonization by electrifying mining equipment and shifting to renewable energy sources such as hydrogen and biomass. Currently only 0.5% of mining equipment is fully electric.

-

Steel manufacturing: Steel is likely to remain a core pillar of the greener economy, as it finds use in renewable energy equipment such as solar thermal pumps and wind turbines. Switching technologies to produce steel exclusively from electric arc furnaces could reduce a steelmakers' cost base. Improving their carbon footprint could also position steel companies well for the European market, where countries aim to renovate the bottom 26% of buildings with the worst energy performance by 2033, kicking off a construction and building wave in the process.

There is already compelling evidence that the market is more willing to place a premium valuation on companies that are making greater transition progress than their peers. Not all heavy emitters will necessarily close the valuation gap given the diversity of their transition approaches, and close analysis is needed to identify the “true improvers,” Martens writes.

|

|

|

| Briefings Brainteaser: Services surge |

|

|

Ireland's services exports grew at a compounded annual rate of 11.4% between 2005 and 2023, the second-highest rate of growth in the world. Which was the only country to surpass Ireland in its service sector's acceleration during this period?

A) India

B) Poland

C) Israel

D) Singapore

Check the answer here. |

|

|

| Goldman Sachs in the news |

|

|

By clicking on these links, you will be redirected to external websites that Goldman Sachs does not own or operate. Goldman Sachs is not responsible for the products, services, or content provided on those sites. Please refer to each external website's terms, privacy and security policies for details. |

|

|

|

Inc. Jun 21 | | For small businesses, a lack of affordable child care stifles growth |

|

|

|

|