The key takeaways today:

- Worries about US consumption are overblown

- What does the rest of 2024 hold for investors?

- A momentum shift in the US equity market

- Global forecast changes: Taiwan's GDP, Saudi Arabia's capex super-cycle

- Should clients stay invested in US stocks?

- Briefings Brainteaser: What is the share of women among CEOs of major US companies?

Was this newsletter forwarded to you? Sign up now. |

|

|

| Can the US consumer stay strong? |

|

|

|

The strength of the US consumer has been one of the hallmarks — and surprises — of this economic cycle. But concerns are rising about the resilience of the US consumer amid high interest rates and lingering inflation, threatening a critical driver of the economic expansion.

David Mericle, Goldman Sachs Research's chief US economist, says most of those concern are overblown. “Strong real income gains plus a positive wealth effect gave us a robust pace of consumption growth last year, and I think it will this year too — just in moderation, because last year was somewhat exceptional,” Mericle says on Goldman Sachs Exchanges. |

|

|

(L to R) David Mericle, chief US economist; Kate McShane, co-lead of consumer sector research; Allison Nathan of Goldman Sachs Research; and Bonnie Herzog, co-lead of consumer sector research |

|

|

While spending is still robust, some consumers are starting to prioritize spending away from discretionary goods and big-ticket items, says Kate McShane, who co-leads coverage of the consumer sector along with Bonnie Herzog. “We have seen strength in consumables, household products, and food, and part of that has to do with the fact that there's been inflation, and so more dollars are going to that. But also you are seeing a prioritization away from discretionary goods, because people are still prioritizing services,” she tells Exchanges host Allison Nathan.

Meanwhile, consumer staples companies are adding more promotions and sales to attract consumers, even as those customers opt for cheaper store brands, Herzog adds. “We are starting to see some of these categories step up in terms of promos to compete and consumers potentially trading down from national brands to these private label or store brands because the price points are typically a lot more affordable.” |

|

|

| What does the second half of 2024 hold for investors? |

|

|

|

Halfway through 2024, investors are contending with a slower-than-expected pace of interest rate cuts, the buildup and fallout of key elections globally, and unfolding megatrends such as AI. In its latest edition of Asset Management Perspectives, Goldman Sachs Asset Management identifies some strategies that may help steer investors through an uncertain second half of 2024.

Hedging for risk: Given multiple sources of risk, an understanding of hedging strategies — including how and when to use them — can potentially prepare portfolios for unexpected events. Strategies include direct hedges, like currency options or credit protection, and indirect diversifying strategies. “Different techniques offer unique advantages and limitations depending on market cycles and risk environments,” write Alexandra Wilson-Elizondo, Goldman Sachs Asset Management's co-chief investment officer of multi-asset solutions, and Oliver Bunn, global head of alternatives for the Quantitative Investment Strategies team.

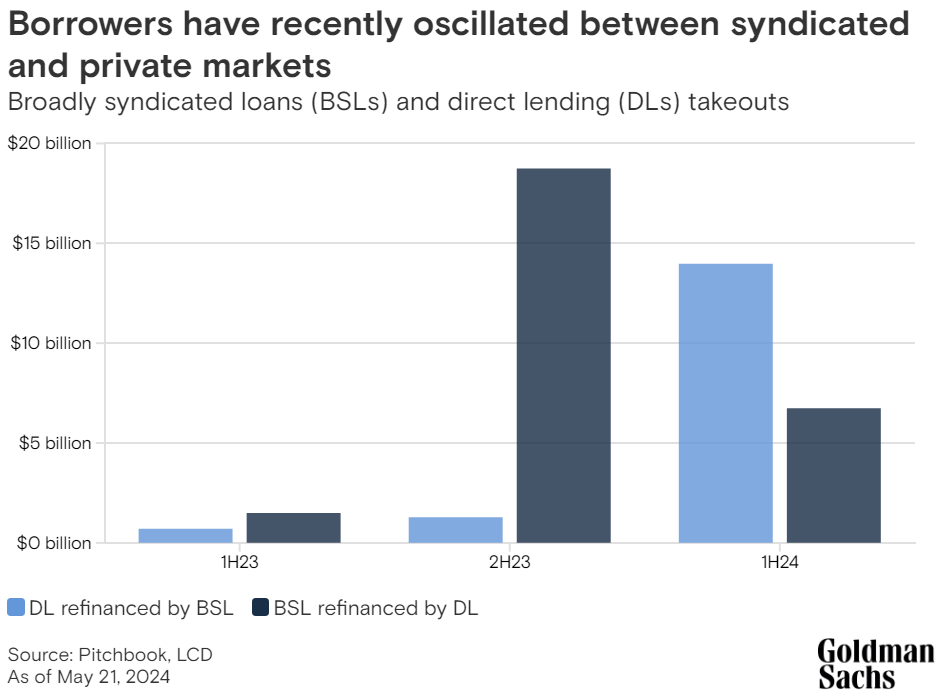

Public and private credit: Public and private credit can serve as complementary elements in portfolios, and new investment opportunities are emerging as companies strategically leverage both markets to secure funding. “Over time, we anticipate an equilibrium where companies will choose between the lower cost of capital available in public markets versus a more tailored capital structure and financing solution in private markets,” write Kay Haigh, global co-head of fixed income and liquidity solutions, and James Reynolds, global head of direct lending for Goldman Sachs Alternatives.

|

|

|

|

US debt: By November, US gross federal debt is expected to have surpassed $35 trillion — a record high that is larger than the size of the US economy. Even so, Goldman Sachs Asset Management doesn't believe US debt dynamics are a near- to medium-term threat to the economy, not least because the US's debt is supported by a unique strength: control over the world's reserve currency. When it comes to investors' appetite for US debt, “we see no signs of a buyers' strike,” writes Candice Tse, global head of the Strategic Advisory Solutions team.

The US election could change the fiscal outlook, though less than one might imagine. A Republican presidency may lead to a continuation of tax cuts, reducing revenue collected by the US to fund its expenses. A Democratic presidency may lead to a similar extension of the tax cuts or an increase in spending that would offset the increase in tax revenues after Trump's tax cuts expire. |

|

|

| The market's momentum shift |

|

|

It's been a terrific year for the momentum trade. But the leadership of the US equity market could be changing, according to Gui Soria, who oversees US factor products within Goldman Sachs Global Banking & Markets.

Momentum simply captures the idea that the equity market's most recent winners will continue to outperform the laggards. Thus far this year, AI optimism has driven the tech giants and a few other top performers, while the higher-for-longer rates narrative has consistently pushed down the shares of smaller and less profitable companies.

|

|

|

But at this point, “both of those themes could be turning around,” Soria says. “We're seeing more skepticism about AI and rates have been declining as we approach a Fed cutting cycle — so it's no surprise that recently we've seen momentum beginning to crack.”

So what does it mean for investors?

“If your portfolio has become over-levered to some of those winners, it might be time to rebalance,” Soria says. He adds that this could mean “picking up small caps, or some of the other under-loved names in the market.” |

|

|

| Global forecast changes: Taiwan's GDP, Saudi Arabia's capex super-cycle |

|

|

↑ Taiwan's GDP: On the back of stronger-than-expected domestic demand, Goldman Sachs Research raised its forecast for Taiwan's GDP growth in 2024 to 4%, from 3.3% previously. Domestic consumption accelerated more than expected, driven by gains in labor income and rapid increases in housing prices. Investment also rose sharply on broad gains across construction, equipment investment, and intellectual property products.

↑ Saudi non-oil investment: Goldman Sachs Research estimates that around 73% of Saudi Arabia's total investments through the end of the decade will be driven by non-oil sectors, up from a previous forecast of 66%. Within the estimated $1 trillion in total investments as part of a “capex super-cycle,” our analysts write, there is an increased focus on clean energy and economic diversification away from oil (towards metals and minerals, for example).

Data as of Aug 1, 2024. |

|

|

| Should clients stay invested in US stocks? |

|

|

US equities have continued to outperform other regions year to date, so Goldman Sachs' wealth management clients are naturally focused on the Investment Strategy Group's view on US equities, asking whether it's time to reduce their exposure. The answer remains a resounding no as the evidence continues to favor staying invested with an overweight to US equities.

ISG's view is underpinned by several factors. The macroeconomic backdrop remains supportive for equities, with continued evidence of slowing inflation and the economy tracking toward ISG's good case of 2.5% growth this year. During past economic expansions, US equity markets have been much more likely to generate a positive return. In fact, since 1945, when the economy was expanding, the S&P 500 has generated a positive total return 86% of the time, and a 20% or greater total return about 30% of the time. Furthermore, ISG believes the Federal Reserve will cut its policy rate in September, which has typically been a tailwind for equities over the following year when the US economy avoided a recession.

|

|

|

Corporate fundamentals are equally supportive. Consensus earnings estimates over the next 12 months have resumed their upward trajectory after declining or stagnating during much of 2022 and 2023, and ISG continues to estimate an 8-10% earnings growth this year. Since the market ultimately follows the path of earnings, improving earnings provide fundamental support to the advance of the S&P 500.

Of course, some of this good news is reflected in today's valuations, which have been cheaper than current levels at least 90% of the time historically. However, history has repeatedly shown that high valuations alone are not a sufficient reason to underweight stocks. The initial price-to-earnings ratio has explained only 6% of the variation in returns over the next year. Moreover, past periods with elevated valuations have still seen substantial subsequent returns, underscoring the penalty for exiting equities prematurely.

ISG also notes that its recommendation to stay invested does not preclude occasional market pullbacks, which can happen at any time. Pullbacks of approximately 5-10% represent normal equity volatility and not a compelling reason to underweight stocks.

Read the full mid-year update of Goldman Sachs' Investment Strategy Group.

|

|

|

| Briefings Brainteaser: Women at the top |

|

|

At the time of the global financial crisis in 2008, the share of women among the CEOs of major US listed companies was less than 2%. A decade and a half later, where does that figure stand today?

A) 0-10%

B) 10-20%

C) 20-30%

D) 30-40%

Check the answer here. |

|

|

| Goldman Sachs in the news |

|

|

By clicking on these links, you will be redirected to external websites that Goldman Sachs does not own or operate. Goldman Sachs is not responsible for the products, services, or content provided on those sites. Please refer to each external website's terms, privacy and security policies for details. |

|

|

|

Bloomberg Jul 26 | | Goldman Sachs' Sharmin Mossavar-Rahmani: US preeminence is intact (6:39) |

|

|

|

|

Barron's Jul 29 | | OpEd by Ashish Shah: A slowing market still has opportunities. Where to look for yield and innovation-driven investments |

|

|

|

|

CNBC Jul 30 | | Goldman Sachs CEO David Solomon on the Olympics, the Fed's rate path, and the M&A landscape (6:31) |

|

|

|

|

Bloomberg Jul 30 | | We're living in a dollar world, says Goldman Sachs' Kamakshya Trivedi (5:57) |

|

|

|

|